Why decentralized compute matters now

The artificial intelligence boom has created a structural bottleneck. Global demand for graphics processing units is projected to grow from $82.68 billion in 2025 to $352.55 billion by 2030, a surge driven by the rapid expansion of large language models and generative AI workloads [1]. This demand is outstripping the capacity of centralized cloud providers, who face physical constraints in data center construction and energy allocation. The result is a pricing environment where traditional cloud GPU rentals have become prohibitively expensive for many developers and startups.

Decentralized physical infrastructure networks (DePIN) offer a structural alternative by aggregating underutilized compute power from distributed hardware owners. Rather than relying on massive, centralized facilities, these networks coordinate real-world resources to form a virtual supercomputer. This model bypasses the capital expenditure hurdles of building new data centers, allowing compute capacity to scale more organically alongside demand.

The economic viability of this model is already evident. In early 2026, the combined market capitalization of DePIN projects surged to $9–10 billion, surpassing the oracle sector [2]. More importantly, these networks generated over $150 million in on-chain monthly revenue, signaling that decentralized compute is generating real economic activity rather than speculative value. This revenue stream validates the infrastructure's ability to serve actual market needs at a lower cost than legacy providers.

The shift toward decentralized compute is not just about cost; it is about resilience. By distributing compute across thousands of nodes, the network becomes less vulnerable to single points of failure that plague centralized cloud architectures.

This macro context sets the stage for a competitive landscape where decentralized GPU marketplaces challenge the dominance of Big Tech. As the gap between AI demand and centralized supply widens, the decentralized model offers a scalable, cost-effective solution that is increasingly difficult for traditional providers to ignore.

Render, Aethir, and Akash: Core players

The GPU market landscape in 2026 is defined by three dominant platforms: Render Network, Aethir, and Akash. While the broader market promises compute resources over four times cheaper than giants like Google Cloud and AWS, these three protocols have carved out distinct niches in enterprise-grade infrastructure. Their value propositions differ in target audience, network architecture, and token utility, creating a competitive triad for decentralized AI training and rendering workloads.

Render Network operates as the established leader in decentralized rendering, leveraging a vast, global network of GPU providers. Its primary focus remains high-performance computing for graphics and AI inference, serving creative studios and AI developers who need scalable, on-demand power. Render’s maturity offers reliability, but its specialized focus on rendering-heavy tasks can limit its flexibility for general-purpose machine learning workloads compared to more open architectures.

Aethir distinguishes itself by targeting enterprise clients with a focus on cloud-native AI infrastructure. It emphasizes low-latency, high-performance computing with a stronger emphasis on service-level agreements (SLAs) and compliance, addressing the reliability hurdles that often block DePIN adoption. By positioning itself as a direct competitor to traditional cloud providers, Aethir aims to bridge the gap between decentralized cost benefits and corporate procurement standards.

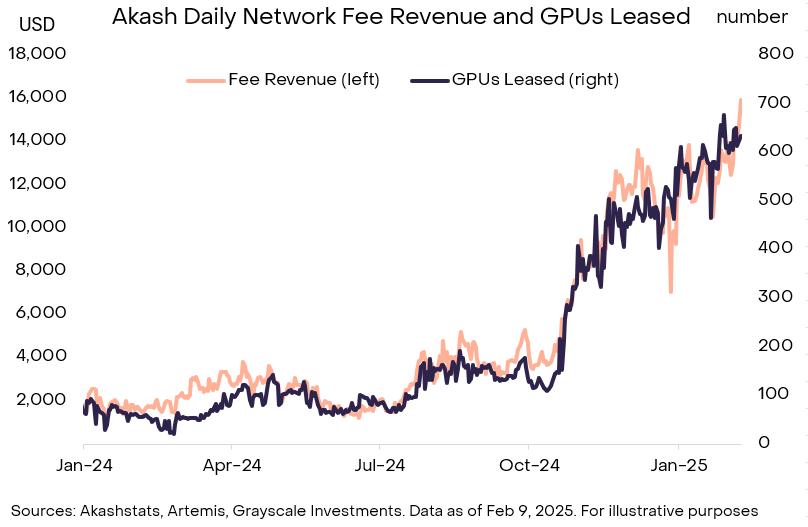

Akash Network takes a more open, marketplace-driven approach, functioning as a decentralized cloud marketplace for all types of compute, not just AI. It allows users to bid for GPU resources, often resulting in significantly lower costs than centralized alternatives. Akash’s flexibility attracts a wide range of users, from individual developers to small startups, prioritizing cost-efficiency and open-source compatibility over enterprise-specific SLAs.

The following table compares the core metrics of these three platforms, highlighting their strategic differences in the 2026 ecosystem.

| Platform | Primary Focus | Target Audience | Market Model |

|---|---|---|---|

| Render Network | Decentralized Rendering & AI | Creative Studios, AI Developers | Service-Specific Marketplace |

| Aethir | Enterprise AI Infrastructure | Enterprises, Cloud Providers | Cloud-Native SLA Provider |

| Akash Network | General Compute Marketplace | Developers, Startups, SMBs | Open Auction Marketplace |

Decentralized compute costs undercut hyperscalers

The economic case for decentralized compute in the GPU market hinges on a stark price differential. Traditional hyperscalers like Amazon Web Services (AWS) and Google Cloud operate with significant overhead, including proprietary hardware margins and centralized data center costs. In contrast, DePIN networks aggregate underutilized compute power from distributed nodes, bypassing these middlemen.

According to market analysis, DePIN projects can provide GPU resources over 4 times cheaper than major cloud providers. This 75% cost reduction is not a marginal discount but a structural advantage that fundamentally alters unit economics for AI training and inference workloads. For developers and enterprises running compute-heavy models, this disparity translates directly into extended runway and higher margins.

| Provider Type | Estimated GPU Hour Cost | Infrastructure Model |

|---|---|---|

| AWS / Google Cloud | High ($1.00 - $4.00+) | Centralized Hyperscaler |

| DePIN Networks | Low ($0.20 - $0.50) | Distributed Node Network |

The gap widens further when considering spot instances and idle capacity. While hyperscalers charge premium rates for guaranteed availability, DePIN networks monetize excess capacity from existing hardware. This dynamic creates a deflationary pressure on compute costs, challenging the pricing power of established tech giants. As AI demand scales, the ability to access cheaper compute becomes a decisive competitive factor.

- Verify spot pricing on major cloud providers before committing to long-term contracts.

- Compare DePIN network uptime guarantees against your application's tolerance for latency.

- Calculate total cost of ownership (TCO) including egress fees, which often differ between providers.

- Test small workloads on DePIN networks to validate performance stability before scaling.

Enterprise adoption barriers and risks

Decentralized compute promises a cheaper alternative to centralized cloud providers, but the path to enterprise-scale migration is blocked by structural reliability gaps. The core issue is not just cost, but the unpredictability of distributed hardware. Unlike dedicated data centers, decentralized GPU networks rely on heterogeneous hardware that may disconnect, overheat, or fail without warning. For finance and healthcare sectors, where uptime is non-negotiable, this volatility creates an unacceptable risk profile for mission-critical workloads.

Service Level Agreements (SLAs) complicate procurement. Traditional cloud vendors offer contractual guarantees with financial penalties for downtime. Decentralized networks currently lack standardized, legally binding SLAs that enterprises can enforce. Procurement teams cannot easily justify migrating sensitive AI training jobs to platforms where recourse for failure is limited to token-based compensation or community governance votes, which are slow and opaque.

Data sovereignty and compliance add another layer of friction. In regulated industries, knowing exactly where data resides is a legal requirement. Decentralized storage and compute often involve data sharding across global nodes, making it difficult to prove compliance with GDPR, HIPAA, or financial data residency laws. Until decentralized networks can provide verifiable, auditable trails for data location and processing, enterprise CIOs will remain cautious.

The market growth projections for GPUs remain strong, but this growth is currently concentrated in centralized hyperscale infrastructure. Enterprises are waiting for decentralized protocols to mature their operational reliability to match the 99.99% uptime standards of AWS or Azure. Until then, DePIN remains a supplementary resource for non-critical tasks rather than a primary compute backbone.

Tokenomics and investment considerations

Decentralized physical infrastructure networks have evolved from speculative experiments into a tangible asset class, with the combined market capitalization of DePIN projects reaching $9–10 billion in early 2026 [[src-serp-1]]. This surge reflects a broader shift in how compute resources are valued, moving away from centralized cloud monopolies toward tokenized models that incentivize hardware deployment. The financial viability of these networks now hinges on the alignment between token utility, liquidity depth, and the actual revenue generated by GPU utilization.

Evaluating Token Utility and Revenue

The primary differentiator for investment consideration is whether a token serves as a governance mechanism or a direct unit of account for compute services. Projects that generate genuine revenue from AI training and inference workloads demonstrate a stronger fundamental base than those relying solely on speculative demand. As the GPU market expands—projected to reach $352.55 billion by 2030—networks that capture even a fraction of this demand through efficient tokenomics offer scalable growth potential [[src-serp-7]]. Investors should prioritize protocols where token burn mechanisms or staking rewards are directly tied to network usage metrics rather than arbitrary inflation schedules.

Market Performance and Liquidity

Visualizing the price action of leading DePIN tokens provides insight into market sentiment and liquidity trends. The following chart illustrates the performance of Render (RNDR), a prominent decentralized compute network, highlighting its correlation with broader crypto markets and AI sector hype cycles.

Liquidity remains a critical risk factor. While DePIN tokens can be purchased on major cryptocurrency exchanges, trading volumes often fluctuate significantly during market downturns. Investors must assess the depth of order books and the stability of staking pools to ensure they can enter or exit positions without substantial slippage. The transition from hype to real revenue, as seen in the latest progress reports from decentralized compute networks, suggests that projects with sustainable token models will outperform those driven purely by narrative [[src-serp-7]].

Risk Assessment

Investing in DePIN tokenomics involves navigating high volatility and regulatory uncertainty. The sector's rapid growth has attracted significant capital, but it also invites scrutiny from financial regulators. Understanding the legal classification of tokens—whether they are securities or commodities—is essential for long-term portfolio management. Additionally, the technical risk of hardware depreciation and network upgrades can impact token value, making thorough due diligence on the underlying infrastructure necessary.

Frequently asked questions about DePIN GPUs

How big is the GPU market in 2030? The global graphics processing unit (GPU) market is projected to expand significantly, growing from USD 82.68 billion in 2025 to USD 352.55 billion by 2030. This trajectory reflects a compound annual growth rate (CAGR) of 33.65%, driven primarily by the escalating demand for artificial intelligence and high-performance computing resources. Source

How to invest in DePIN? Investing in Decentralized Physical Infrastructure Networks (DePIN) typically involves purchasing DePIN tokens on various cryptocurrency exchanges. These platforms serve as the primary venues for trading these digital assets, allowing investors to gain exposure to projects that provide real-world services like GPU compute, storage, or connectivity. Source

What distinguishes DePIN GPUs from traditional cloud providers? DePIN networks operate on a decentralized model where individual node operators contribute idle GPU capacity to a shared pool. Unlike centralized cloud giants, this structure aims to lower costs through competition and reduce single points of failure. Projects succeed when they provide tangible utility, such as rendering or AI inference, ensuring long-term demand for the underlying hardware. Source

No comments yet. Be the first to share your thoughts!