The 2026 decentralized compute surge

The decentralized physical infrastructure network (DePIN) sector has crossed a significant financial threshold in early 2026. The combined market capitalization of DePIN projects has surged to $9–10 billion, a milestone that signals a transition from speculative hype to tangible revenue generation. This growth outpaces other infrastructure sectors, including oracles, as institutional capital increasingly recognizes the utility of decentralized compute.

At the core of this expansion is the GPU marketplace. These platforms are no longer just theoretical experiments; they are generating approximately $150 million in monthly on-chain revenue. This financial performance demonstrates that decentralized networks can reliably aggregate idle GPU power and match it with demand from AI training, rendering, and scientific computing workloads.

The shift toward decentralized compute is driven by the limitations of centralized cloud providers. As demand for compute hours escalates, the traditional model struggles with capacity constraints and opaque pricing. DePIN networks offer a more granular approach to resource allocation, allowing users to bid for specific SLAs (Service Level Agreements) while providers earn yield from otherwise idle hardware. This tokenomics model aligns incentives, creating a resilient infrastructure layer that competes directly with Big Tech data centers.

DePIN Compute Costs vs. Big Tech Clouds

The primary economic driver for Decentralized Physical Infrastructure Networks (DePIN) is the significant reduction in compute costs compared to traditional hyperscalers. By leveraging global surplus hardware and idle GPU capacity, DePIN networks can offer resources at a fraction of the price charged by AWS or Google Cloud. Industry analysis indicates that DePIN projects can provide GPU resources over 4 times cheaper than these established giants, a disparity driven by lower overhead and the elimination of proprietary hardware margins.

To understand the scale of this advantage, it is necessary to compare the operational metrics that matter to enterprise buyers: cost per hour, availability guarantees, and service level agreements (SLAs). The following table contrasts the typical pricing and reliability structures of leading DePIN networks against major cloud providers.

| Provider | Est. Cost per Hour (A100) | Availability Model | SLA Guarantee |

|---|---|---|---|

| AWS / Google Cloud | $3.00 - $4.50 | Centralized Data Centers | 99.9% - 99.99% |

| Render Network | $0.80 - $1.20 | Global Distributed Nodes | Variable (Network Dependent) |

| Akash Network | $0.50 - $0.90 | Open Cloud Marketplace | 99% - 99.9% |

| Io.net | $0.60 - $1.00 | Consumer/Prosumer GPUs | Best Effort |

While the cost savings are substantial, they come with trade-offs in consistency. Big Tech providers offer predictable, high-uptime environments backed by massive capital expenditures, whereas DePIN networks rely on a diverse, often fragmented, hardware base. For training large language models where interruptions can be managed, DePIN offers a compelling arbitrage. However, for latency-sensitive inference or mission-critical workloads, the variable nature of decentralized availability requires careful architectural planning and robust tokenomics to ensure long-term resource stability.

Frequently asked: what to check next

Leading decentralized GPU networks

The decentralized compute sector has consolidated around three primary infrastructure providers: Render, Aethir, and Akash. Each network targets a distinct segment of the GPU market DePIN, offering specialized hardware configurations and tokenomics designed to compete with centralized cloud giants. Their combined market capitalization has reached approximately $9–10 billion in early 2026, signaling a structural shift in how AI training and rendering workloads are procured.

Render: Distributed Rendering and AI

Render Network operates as a distributed GPU cluster focused on high-performance rendering and, increasingly, AI inference. By aggregating idle GPU power from individual node operators, Render provides a cost-effective alternative to AWS or Azure for 3D rendering farms and generative AI tasks. The network’s tokenomics are tied directly to compute hours consumed, ensuring that node operators are compensated based on actual hardware utilization rather than speculative staking rewards. For studios and AI developers, Render offers a scalable pool of resources that bypasses the provisioning delays typical of traditional cloud providers.

Aethir: Enterprise-Grade AI Training

Aethir distinguishes itself by targeting enterprise clients requiring low-latency, high-throughput AI training. Unlike consumer-focused networks, Aethir curates a supply chain of premium data center GPUs, ensuring the stability and performance guarantees (SLAs) necessary for large-scale model training. The network’s architecture prioritizes reliability, allowing enterprises to run sensitive workloads without the risk of node downtime. This focus on institutional-grade infrastructure positions Aethir as a direct competitor to centralized hyperscalers, particularly for companies requiring guaranteed compute availability for complex machine learning tasks.

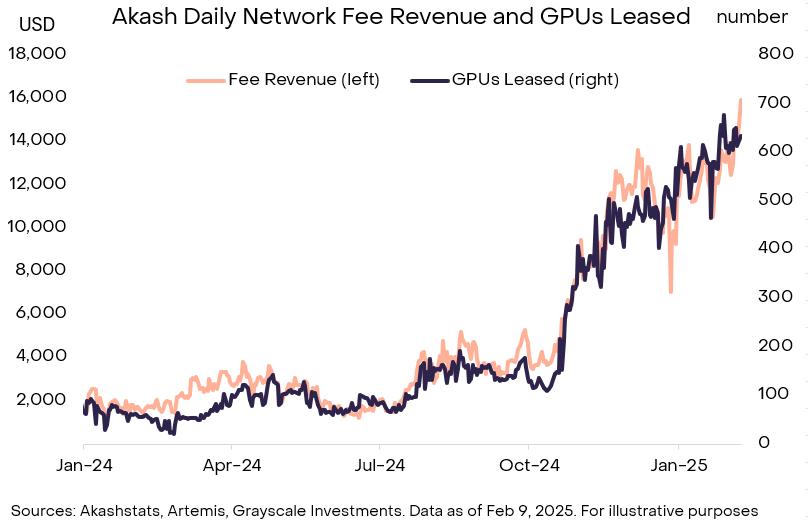

Akash: Open-Source Cloud Marketplace

Akash Network functions as an open-source, decentralized cloud marketplace, often described as the "Airbnb of cloud computing." It supports a wide variety of workloads, from containerized applications to large-scale AI training jobs, by leveraging underutilized data center capacity. Akash’s competitive advantage lies in its pricing model, which typically undercuts centralized providers by 50–80% due to its open-market auction mechanism. Node operators bid to host workloads, driving down costs for users while maintaining a transparent, on-chain record of all transactions. This flexibility makes Akash a preferred choice for startups and developers seeking to minimize infrastructure overhead.

Token Price and Market Context

The financial health of these networks is reflected in their native token performance. Investors and users should monitor the live market data for RNDR, ATH, and AKT to assess current valuation trends and liquidity conditions.

Enterprise adoption barriers

Decentralized compute offers a compelling price advantage, yet the path to enterprise migration is obstructed by significant reliability and operational risks. While DePIN networks promise lower costs per compute hour, they currently lack the standardized Service Level Agreements (SLAs) that financial and healthcare sectors require for mission-critical workloads.

Reliability variance remains the primary technical hurdle. Big Tech providers guarantee 99.99% uptime through redundant, centralized data centers. In contrast, decentralized GPU clusters depend on heterogeneous hardware and varying network conditions. A single node failure can interrupt a training job, causing data loss or requiring expensive re-computation. This unpredictability makes it difficult for enterprises to commit long-term resources without hybrid safeguards.

SLA gaps further complicate procurement. Traditional cloud contracts offer legal recourse for downtime, whereas DePIN tokenomics often rely on smart contract penalties that may not cover indirect business losses. Procurement teams are hesitant to approve vendors who cannot provide indemnification or clear liability frameworks for data sovereignty issues.

Until these structural issues are resolved, enterprises will likely adopt a hybrid approach, using DePIN for non-critical inference tasks while reserving Big Tech infrastructure for core AI training.

Emerging markets drive DePIN growth

The 2026 DePIN wave is shifting from Silicon Valley to Nairobi, Manila, and Medellín. This geographic diversification lowers infrastructure costs and expands the global compute supply chain. Emerging markets offer lower electricity rates and favorable regulatory environments, making them ideal for high-density GPU clusters.

Providers in these regions are securing long-term SLAs with enterprise clients, ensuring stable revenue streams. The tokenomics of these networks favor local node operators, creating a self-sustaining ecosystem. This decentralization reduces reliance on single-region data centers, mitigating geopolitical and operational risks.

No comments yet. Be the first to share your thoughts!