DePIN vs Big Tech GPU Pricing

The structural difference between centralized cloud providers and decentralized networks defines the current GPU market dynamic. Big Tech companies like Amazon Web Services (AWS) and Google Cloud maintain pricing power through monopoly-like control over high-end hardware. Decentralized Physical Infrastructure Networks (DePIN) disrupt this model by aggregating idle or underutilized GPU capacity from individual providers and small data centers. This fragmentation creates a competitive pressure that centralized giants cannot easily match without sacrificing margins.

This price gap is not temporary; it is baked into the economic structure of both models. Centralized providers bundle infrastructure costs, energy overhead, and significant profit margins into their hourly rates. Decentralized networks operate on a spot-market logic, where node operators set prices to compete for compute tasks. The result is a transparent, lower-cost baseline for AI training and inference workloads.

For financial decision-makers, this shift represents a move from capital-intensive infrastructure ownership to flexible, variable-cost consumption. The DePIN market cap currently stands at approximately $9.19 billion, reflecting steady growth as enterprises seek alternatives to volatile cloud pricing. While NVIDIA dominates the hardware supply with 94% of the AIB GPU market share, the distribution layer is becoming increasingly decentralized.

The economic thesis is simple: if you can access the same compute power for a fraction of the cost, the barrier to entry for AI development lowers. This efficiency gain is the primary driver behind the rapid adoption of decentralized compute solutions in 2026.

Top Three GPU Rental Networks

The decentralized GPU market has consolidated around three primary protocols that serve distinct segments of the AI and rendering workload spectrum. Render, Aethir, and Akash dominate the landscape, each offering a different structural approach to compute aggregation. Understanding their specific architectures is essential for selecting the right network for high-stakes compute needs.

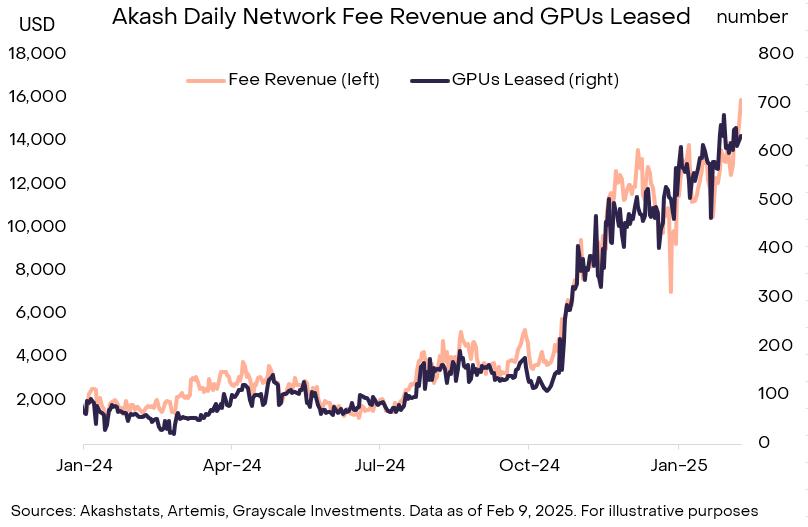

Render operates as the first decentralized GPU rendering platform, initially built for artists but now scaling to high-performance AI inference. Its network relies on a specialized node infrastructure designed for visual computing, making it a strong candidate for graphics-intensive tasks. Aethir focuses on cloud gaming and AI training by aggregating enterprise-grade data center GPUs, offering lower latency for real-time applications. Akash provides a general-purpose decentralized marketplace, functioning as an open-source alternative to traditional cloud providers with a flexible, bidirectional auction model.

The following table compares their core operational differences, pricing structures, and token utility mechanisms.

| Protocol | Primary Use Case | Pricing Model | Token Utility |

|---|---|---|---|

| Render | 3D Rendering & AI Inference | Fixed Node Rates | Network Fees & Staking |

| Aethir | Cloud Gaming & AI Training | Enterprise Contracts | Access & Governance |

| Akash | General Compute & Hosting | Bidirectional Auctions | Gas & Collateral |

Enterprise Barriers to Adoption

The structural dominance of centralized cloud providers is not merely a matter of brand recognition; it is a function of entrenched procurement and operational workflows. For large enterprises, the risk calculus favors the known entity. NVIDIA’s recent consolidation of the AIB GPU market share to 94% in Q4 2025 underscores the sheer scale of capital required to compete in hardware supply chains [src-serp-8]. This monopoly creates a high barrier to entry, as decentralized networks must not only match performance but also overcome the logistical inertia of existing vendor contracts.

Reliability remains the primary technical hurdle for DePIN adoption. Enterprise SLAs (Service Level Agreements) demand guaranteed uptime and latency consistency that distributed, volunteer-driven hardware struggles to provide. While decentralized compute offers significant cost advantages, the variability of consumer-grade GPUs introduces operational friction. CIOs are hesitant to migrate critical AI workloads to networks where node availability is probabilistic rather than contractual. The gap between "good enough" for experimental models and "guaranteed" for production inference is currently wide.

Procurement processes further slow adoption. Traditional IT departments require standardized invoicing, tax compliance, and liability frameworks that decentralized protocols often lack. Integrating DePIN requires new legal structures and risk management protocols, creating a significant administrative burden. Until these networks can offer enterprise-grade support and financial instruments comparable to AWS or Azure, they will remain confined to non-critical, experimental workloads.

GPU Market DePIN Size and Token Performance

The DePIN sector has established a measurable financial footprint, currently valued at approximately $9.54 billion according to CoinGecko. This capitalization reflects the aggregate value of tokens representing decentralized compute, storage, and sensor networks. While the sector experiences daily volatility, the underlying asset class demonstrates significant liquidity and institutional interest.

Render (RNDR) remains the primary benchmark for GPU-centric DePIN valuation. Its price action often dictates the sentiment for the broader decentralized compute sector. The following chart illustrates the recent trading range for RNDR, providing context for how token performance correlates with demand for decentralized rendering and AI inference capacity.

Other major players like Aethir (ATH) and io.net contribute to the sector's depth, though with lower market caps than Render. Investors track these tokens to gauge the health of specific niches within the GPU market, such as real-time rendering versus large-scale AI training clusters. The divergence in performance between these tokens highlights the maturation of the sector, where utility-driven demand begins to separate leading projects from speculative assets.

Key Considerations for Investors

Who are the major players in DePIN?

The DePIN sector is dominated by specialized protocols rather than generalist platforms. In the GPU compute space, Aethir, Render, and Akash currently hold the most significant market positioning. Each protocol serves distinct use cases, ranging from high-performance AI training clusters to scalable rendering farms, creating a fragmented but competitive landscape for enterprise buyers.

What are examples of successful DePIN projects?

Beyond GPU compute, several DePIN projects have established functional networks. Render Network and io.net are leaders in distributed graphics processing. Other notable examples include Helium for wireless connectivity, Hivemapper for mapping data, and Nosana for specialized compute tasks. These projects demonstrate the viability of token-incentivized infrastructure models.

Who is the leader in the GPU market?

NVIDIA maintains a near-monopoly on the discrete GPU market. According to Q4 2025 data from Jon Peddie Research, NVIDIA holds 94% of the Add-In Board (AIB) market share, while AMD has fallen to 5%. This concentration highlights the structural dependency of DePIN networks on centralized hardware supply chains.

What is the market cap of DePIN?

The total market capitalization for the DePIN sector fluctuates with broader crypto market trends. Recent data indicates a market cap around $9.19 billion to $9.54 billion. Investors should monitor these figures alongside individual protocol performance to assess sector health.

No comments yet. Be the first to share your thoughts!